Bitcoin Consulter™

Bitcoin Taxable Events

Cryptocurrency is a relatively new concept:

And crypto-taxation is an even newer concept.

That’s why it might take some time before people get used to the tax laws and all the confusion surrounding the crypto space. Until then, it’s always a good idea to consult a tax professional when in doubt.

Update 01-15-2026 @ Block Height: 932410

How The Rich Live On Loans

Living on loans is supposed to ruin your life. That is.. Unless you are rich.

Buy Borrow Die: The Free Money Loophole Available Only For The Rich.

Understanding Retirement on Bitcoin Without Selling or Borrowing?

You’re spot on about the tax angle: Loans against Bitcoin (BTC) as collateral aren’t taxable events, unlike selling, which triggers capital gains taxes (up to 20% long-term in the US, depending on your bracket). Platforms like Ledn, Nexo, or Aave let you borrow USD or stablecoins at low loan-to-value (LTV) ratios (e.g., 30-50%) to minimize liquidation risk if BTC’s price drops.

But as you noted, in retirement with only Social Security Administration (SSA) benefits (averaging ~$1,900/month in 2025), covering loan interest (often 5-10% APR) plus living expenses requires some cash flow—without active income, you’d eventually need to sell BTC or risk default.

The good news? Yes, there are ways to generate sustainable income from your BTC holdings without selling a single satoshi or taking on debt to repay. These rely on Bitcoin’s ecosystem for passive yield (earning more BTC or equivalent value over time).

However, BTC isn’t like dividend-paying stocks—it’s not designed for native yield—so these methods often involve wrapped BTC (e.g., WBTC on Ethereum) or layer-2 solutions. Yields are variable (typically 1-6% APY as of late 2025), influenced by market demand, and come with risks like smart contract bugs or platform hacks.I’ll break it down into viable strategies, pros/cons, and real-world examples.

These can supplement SSA to cover gaps (e.g., if you need $4,000/month total, aim for $2,100 from yield). Always DYOR, start small, and consult a tax advisor—yields may be taxable as income.1. Lending Your BTC for Interest (CeFi or DeFi)

- How it works: Deposit BTC into a lending platform where borrowers pay interest to use it (e.g., for trading or margin). You earn ~2-5% APY in BTC or stablecoins, paid periodically. No selling or borrowing on your end—you’re the lender.

- No repayment needed: The interest is your income stream. Withdraw it as cash (via stablecoins) for bills, while your principal BTC stays intact.

- Platforms:

- CeFi (centralized, easier for beginners): Nexo (up to 5% on BTC), Ledn (3-4%), or BlockFi successors like Gemini Earn (2-3%). Custodial, so they hold your keys—lower risk for newbies.

- DeFi (decentralized, self-custodial): Use wrapped BTC (WBTC) on Aave or Compound for 1-4% APY. Tools like Babylon (Bitcoin staking protocol) let you earn without wrapping.

- Example: With 1 BTC (~$95,000 in Sep 2025), at 4% APY, you’d earn ~0.04 BTC/year ($3,800)—enough for extras like groceries or travel, on top of SSA.

- Pros: Simple, liquid (withdraw anytime), compounds if reinvested.

- Cons/Risks: Platform insolvency (e.g., past Celsius collapse); BTC price volatility erodes yield value; DeFi gas fees.

2. Bitcoin Staking and Liquid Staking

- How it works: “Stake” BTC to secure networks (via protocols like Babylon or Stacks layer-2), earning rewards in BTC or tokens (~1-3% APY). Liquid staking (e.g., via stBTC) gives you a tradable token representing your staked BTC, so it’s not locked.

- No repayment needed: Rewards accrue as passive income—claim and convert to fiat/stablecoins for spending.

- Platforms: Babylon Finance (native BTC staking, 2-3% APY); Core DAO (Bitcoin-powered staking, ~1.5%); or liquid options like Solv Protocol.

- Example: Stake 0.5 BTC ($47,500) at 2.5% APY = ~0.0125 BTC/year ($1,190). Scale up as your stack grows.

- Pros: Keeps full BTC exposure; supports Bitcoin’s network (aligns with HODL ethos).

- Cons/Risks: Lower yields than altcoins; slashing penalties if the network faults (rare); emerging tech, so audit reports are key.

3. Yield Farming with BTC Liquidity Pools

- How it works: Provide BTC (or WBTC) liquidity to decentralized exchanges (DEXs) like Uniswap or Curve. Earn a share of trading fees + protocol rewards (~3-6% APY, sometimes higher in bull markets).

- No repayment needed: Fees and tokens are your yield—harvest and sell for cash flow.

- Platforms: Yearn.finance (auto-optimizes BTC farms for 4-5%); Convex Finance (boosted yields on Curve BTC pools).

- Example: Farm 0.2 BTC in a WBTC/ETH pool at 5% APY = ~0.01 BTC/year ($950). Use low-risk stablecoin-BTC pairs to avoid impermanent loss.

- Pros: Higher potential returns; diversified if you mix with stablecoins.

- Cons/Risks: Impermanent loss (if BTC price swings vs. paired asset); smart contract exploits; more complex (use wallets like MetaMask).

Quick Comparison Table: Yield Strategies for BTC Retirement

| Strategy | Est. APY (2025) | Ease of Use | Risk Level | Best For | Example Monthly Income (on 1 BTC) |

|---|---|---|---|---|---|

| Lending (CeFi/DeFi) | 2-5% | High | Medium | Beginners | $160-400 |

| Staking | 1-3% | Medium | Low-Medium | HODLers | $80-250 |

| Yield Farming | 3-6% | Low | High | Advanced | $250-500 |

Assumptions: BTC at $95K; yields variable; income convertible to USD via exchanges like Coinbase.Realistic Path for SSA-Only Retirees

- Step 1: Build a “yield engine.” If you have 0.5-1 BTC, start with low-risk lending (e.g., Nexo) for immediate 3% (~$1,400/year on 0.5 BTC).

- Step 2: Layer in staking for growth. Use SSA to cover basics; yield for discretionary spending.

- Step 3: Monitor & adjust. Tools like DeFiLlama track real-time APYs. Aim for 4% safe withdrawal rate (like the 4% rule for stocks) to avoid depleting principal.

- Tax note: Yields are ordinary income (taxed at your bracket, ~22% average), but no cap gains. In a Roth IRA via Fidelity Crypto, it could grow tax-free.

The Caveats: Is This “Truly” Sustainable?These methods do work without selling or debt repayment—the yield covers your outflow. But BTC’s volatility means a 50% price crash could halve your income’s fiat value overnight. Historical data shows BTC’s long-term CAGR ~60% (outpacing yields), so holding principal pays off.

If yields drop to 1%, you’d need a larger stack (e.g., 2 BTC for $1,900/year at 1%).Podcasts like “What Bitcoin Did” or “The Investor’s Podcast” often cover this (search episodes on “Bitcoin yield” or “retiring on sats”). For deeper dives, check Reddit’s r/Bitcoin threads on passive income—they echo your concerns but highlight lending/staking success stories.

If BTC hits $200K+ by 2030 (as some models predict), even modest yields could fund a lavish retirement. Start small, diversify platforms, and never risk what you can’t lose. What’s your BTC stack looking like, or which method intrigues you most?

Selling Crypto for Fiat Currency?

Before we start talking about the various crypto taxable events, first, we must understand the foundation of it all, and it begins with understanding how the IRS views crypto. As per IRS guidelines, crypto is treated as “property.” Therefore, selling crypto for fiat currency is considered disposing of a capital asset. Hence, tax rates for crypto are the same as tax rates for capital gains/losses.

There are two factors that influence the capital gains tax rate – Income and Holding period.

If the holding period of your asset (crypto) is less than 365 days, you’ll have to pay the short-term capital gain tax rate, which ranges between 10%-37%, based on income level. On the other hand, if the holding period is more than 365 days, you’ll pay a long-term capital gain tax rate, ranging between 0-20%.

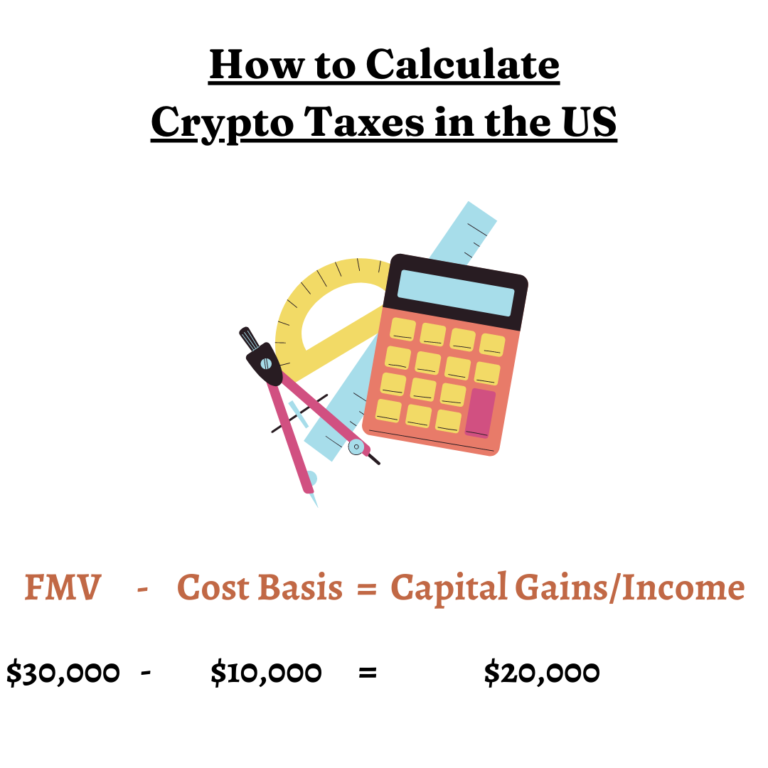

How to Calculate Capital Gains/Losses?

The simple formula for calculating your capital gains and losses is this Cost Basis – Fair Market Value (FMV) of the Coin = Capital Gain/Loss

Cost basis refers to the amount you paid for incurring a coin, and the fair market value represents the price you sold that coin for or the price it would generally sell in the market at that point in time. Subtracting the cost basis from the fair market value will give you your capital gain/loss.

Consider the following scenarios to understand the entire concept better.

Scenario 1

You buy 1 BTC for $1000 in January 2015 – You sell it for $5000 in September 2021

Is that 1 Bitcoin taxable now?

Yes, in this scenario, you will realize a long-term capital gain of $4000 since the holding period was more than 365 days.

Scenario 2

You buy 1 BTC for $5000 in February 2021 – You sell it for $5500 in September 2021

In this scenario, you will realize a short-term capital gain of $500 since the holding period was more than 365 days.

There are many more variations to this, which we will explore more in this article. But this was the foundation of crypto taxation that you must understand to grasp the concept of the rest of the taxable events.

However, if you’re someone who finds the entire process of going through transactions, calculating taxes, and getting all the required data to report them to the IRS a headache, then consider using Bitcoin.Tax. Just upload or add all the transactions directly from the exchanges and wallets you use, along with any crypto you might already own and Bitcoin.Tax will take care of the rest. It will calculate your capital gains and produce the required data and forms you need to file your taxes.

Crypto as Gifts?

Receiving crypto as gifts doesn’t make any significant difference to how the IRS views them. It’s still a crypto taxable event, and the same capital gains tax rate will apply to gifts as well, but only if the gift passes the $15,000 threshold, in which case, the receiver will inherit the cost basis of the coin. However, gifts under the $15,000 threshold are free from taxes in the US. Laws in other countries may vary.

Trading One Cryptocurrency for Another?

Some people get confused about whether trading one cryptocurrency for another is a crypto taxable event or not since you’re not selling your crypto for fiat currency. However, that’s not the case. As per IRS guidelines, when trading one crypto for another, you’re technically disposing of your cryptocurrency and buying another one. In this case, the fair market value of the crypto you dispose of would be the cost basis for the crypto you traded it for. Confusing? Let’s see an example to understand it better, and for the sake of simplicity, we won’t involve the holding periods for these cryptos.

You buy 1 BTC for $1000 – You then trade it for 5 ETH, and at the time of trading, the FMV of 1 BTC is $2000 – You realize a capital gain of $1000

In this scenario, you’ll be actually disposing of the 1 BTC to buy 5 ETH, and since the FMV of 1 BTC at the time of disposing of is more than the cost basis, you’ll realize a capital gain. At the same time, the FMV of the 1 BTC will now be considered the cost basis of the 5 ETH.

However, this was not always the case. Prior to 2018, trading one crypto for another wasn’t a taxable event since the tax laws at that time weren’t clear for these kinds of transactions. So, if you’re still filing your taxes from 2017 and before, you don’t need to report crypto-to-crypto trades.

Buying Products/Services with Crypto?

Buying something or paying someone with crypto is becoming more and more common these days. However, very few people know the tax consequences of paying with crypto. To explain how buying something could be a crypto taxable event, let’s look at some examples.

Suppose you bought 0.5 BTC for $500. You then use it to buy a new pair of headphones worth $800. Now, by applying the usual capital gains logic, you’ve realized a capital gain of $300.

However, what happens when you don’t know the worth of a product or service. Let’s look at another example.

Suppose you bought 0.5 BTC for $500. You then hire someone to drive your car who charges 0.5 BTC for his services. In this scenario, if the FMV of the 0.5 BTC is more than its cost basis, let’s say $600, you’ll once again realize a capital gain of $100.

Buying NFTs?

Despite no apparent guidelines from the IRS, most people consider NFTs as collectibles, and collectibles are subject to capital gain tax rates. Therefore, buying NFTs is almost the same as trading one crypto for another.

Getting Paid with Crypto?

Taxes on getting paid with crypto are pretty simple and straightforward. You pay ordinary income tax rates on the equivalent amount of money that the crypto you receive as payment is worth.

For example, say your wage is $2000 per month, and instead of getting the pay in your fiat currency, you receive the equivalent worth of crypto. In that case, you would still be taxed for only $2000 under ordinary income tax rates.

Similarly, if your wage is 50 BTC per month, then you’ll have to pay the income tax rates on the FMV of the 50 BTC at that time. That’s why you must keep detailed records of all this information.

There are some other similar scenarios where the same logic applies, such as –

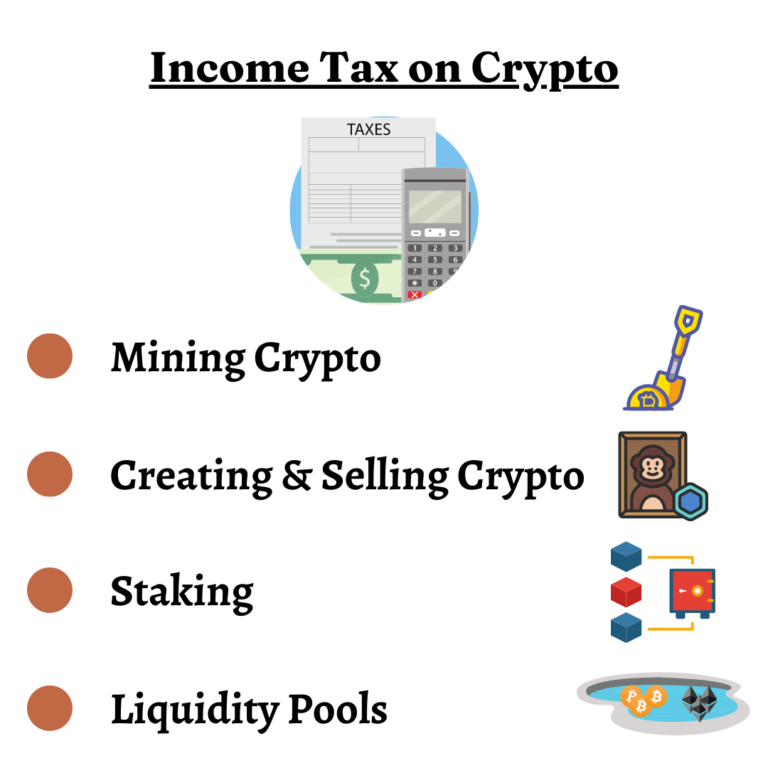

Mining

Miners earn rewards for completing their tasks in crypto. That’s why miners must pay ordinary income tax rates and self-employment tax rates on their earnings. And since you’ll be filing self-employment taxes as well, you’re allowed to deduct business expenses such as equipment costs and electricity costs.

Further, selling the earned cryptocurrency will trigger another taxable event – capital gains taxes.

Staking

Although staking may seem different from mining and selling NFTs on the surface, the tax implications are pretty much the same. Interests earned from staking your coins will be treated as your ordinary income. Therefore, ordinary income tax rates also apply to staking.

Further, selling the earned cryptocurrency will trigger another taxable event – capital gains taxes.

Liquidity Pools

Similar to staking, interest earned from liquidity pools is also subject to ordinary income tax rates, and further, selling the earned cryptocurrency will trigger another taxable event – capital gains taxes.

On a side note, though, putting your crypto in liquidity pools may or may not be a crypto taxable event, as some platforms provide a different token in exchange for the original one. In that case, it could be viewed as disposing of your assets (crypto), hence a taxable event.

However, it’s not always the case, as some platforms work differently. The lack of clear guidelines from the IRS on DeFi only adds to the confusion. That’s why it’s best to consult your tax professional before getting involved.

Non-Taxable Events

Now that we have talked about all the possible crypto taxable events. Let’s talk about transactions that may seem taxable on the surface but actually aren’t. These are either exceptions or loopholes in the system that allow people to avoid taxes.

Taxes on Crypto Loans & Collaterals

Generally speaking, taking loans is not a taxable event in itself. What’s even more important and confusing for some people is collateral. When using your crypto as collateral against a loan, you aren’t actually disposing of your coins. Therefore, there are no tax implications for it.

There are exceptions, though, such as paying back the interest, which is a taxable event, or if you don’t pay back the loan, the platform may dispose of your collateralized asset (crypto), which is again a taxable event. However, mostly taking loans and using your cryptocurrencies as collateral are not taxable.

Cryptocurrency Swaps

The IRS has not provided any specific guidelines regarding crypto swaps. However, based on existing guidelines, it’s safe to assume that crypto swaps are not a taxable event. Though, it’s important to keep a record of the cost basis of the previous crypto to calculate the cost basis of the new one because that’s essential to calculate the capital gain/loss when you sell it in the future.

For example, suppose you’ve bought 5 VEN for $500 (500/5= $100 per VEN), but after the swap, you get 50 VET in exchange for 5 VEN (10 VETS = 1 VEN). So, based on the cost basis of VEN, we can calculate the cost basis of 1 VET, which would be $10 (Cost basis of VEN – $100/10 VETS = $10). Some people may find this very complicated, and that’s why there are crypto tax calculator tools out there that you can use to simplify all of this, like Bitcoin.Tax.

What if your Crypto Gets Lost or Stolen?

Recovering losses on lost or stolen crypto is not the most straightforward task. But it can significantly help your case if you possess detailed info and records of all your transactions, dates, amounts, when and how the assets got stolen or lost, etc.

You can check out the 26 U.S. Code § 165 – Losses for more information on if you can recover your losses and how. Nonetheless, you should always keep detailed records of all the important data and transactions, which brings us to the last segment of this article.

The Importance of Keeping Records

Not only is it essential to keep records for calculating your taxes and providing evidence for them, but keeping detailed records can tremendously make the process of reporting your taxes easier and faster. If you don’t want a headache while filing your taxes, you might want to consider keeping records of all the taxable events that occurred while doing crypto-related transactions.

Creating & Selling NFTs

NFT artists and creators who create and sell NFT artwork will also have to pay ordinary income tax rates on their earnings. Similar to mining, NFT artists can also deduct business expenses.

Further, selling the earned cryptocurrency will trigger another taxable event – capital gains taxes.

Bitcoin Taxable Events: Don’t let your lack of knowledge hold you back from investing in Bitcoin.

Ready for Full Sovereignty?

Bitcoin belongs to everyone. Claim yours securely — no banks, no middlemen.

Start now.

Bitcoin Consulter™

Bitcoin Consulter™ offers training, support, and best practices to help independent Bitcoiners worldwide strengthen their sovereignty and navigate their Bitcoin journey.

FREE BITCOIN ART

Subscribe — stay ahead with BTC news, deals & new lessons.

FOLLOW US

Established @ Block Height : 449,049

©2026 Bitcoin Consulter™ – Privacy | Terms